There are two tax credits available to help you offset the costs of higher education by reducing the amount of your income tax; these are the American opportunity credit and the lifetime learning credit. The taxpayer will need to decide which credit they are eligible to receive.

The American opportunity credit is up to $2,500 for qualified education expenses paid for each eligible student.

- A tax credit reduces the amount of income tax you may have to pay. Unlike a deduction, which reduces the amount of income subject to tax, a credit directly reduces the tax itself.

- Your allowable American Opportunity Credit may be limited by the amount of your income.

- Generally, you can claim the American Opportunity Credit if all three of the following requirements are met.

- You pay qualified education expenses of higher education.

- You pay the education expenses for an eligible student.

- The eligible student is yourself, your spouse, or a dependent for which you claim an exemption on your tax return.

The Lifetime Learning Credit is based on qualified education expenses you pay for yourself, your spouse, or a dependent for which you claim an exemption on your tax return. Generally, the credit is allowed for qualified education expenses paid in the current tax year for an academic period beginning in the current tax year or in the first 3 months of the following tax year. You may claim the Lifetime Learning Credit if all three of the following requirements are met.

- You pay qualified education expenses of higher education.

- You pay the education expenses for an eligible student.

- The eligible student is yourself, your spouse, or a dependent for which you claim an exemption on your tax return.

Temple University is required to provide all students with a 1098-T tax form that records certain required information.

Federal 1098-T forms are distributed by January 31 each year to students who meet the Internal Revenue Services’ reporting requirements. Students can choose electronic delivery or by mail to the student’s permanent address of record. In order to receive a 1098-T form, students must have an active permanent address to be reported to the IRS.

Currently enrolled students can access 1098-T information and transaction details in TUpay by selecting TCS1098-T:

Former students can access forms at: www.tsc1098t.com

Enter the following information:

- Site ID: 11432

- Username: Temple Student ID beginning with 9

- Password: last 4 digits of your SSN (unless you already logged in and changed your password)

- Once logged in, select "View/Print My 1098-T"

Students entitled to receive a Federal 1098-T tax form for the Hope Scholarship/Lifetime Learning Credit will be notified by Temple. Once you receive notification, please sign up to receive your form electronically.

Enrolling in this service will allow quicker delivery with the ability to print multiple copies for yourself, your parents, or your tax Once you have enrolled, you will receive an email notification when your form is available.

If you take advantage of this feature, you will have access to your tax form approximately 2-3 weeks sooner.

To enroll for this service, visit www.tsc1098t.com and enter the following information:

- Site ID: 11432

- Username: Temple Student ID beginning with 9

- Password: last 4 digits of your SSN (unless you already logged in and changed your password).

Once logged in, the "Consent to receive your 1098-T electronically" page will be displayed. Please read the information thoroughly, scroll to the bottom, select "Accept Consent" and then click submit.

FAQ's

What is a 1098-T form?

The IRS requires Temple to report, both to the student and the IRS, certain summary financial information for students who meet IRS reporting criteria. This information is provided to assist students in determining their eligibility for certain educational tax credits.

This includes the following for transactions posted to student accounts in the previous tax year:

- Payments received for tuition & qualified fees

- Information on non-student/family payments and loans, including:

- Temple administered grants & scholarships

- External/private scholarships

- Third party payments made by sponsors billed by the University on behalf of the student

The IRS now requires Temple to report payments received for qualified tuition and fees and university administered grants and scholarships.

Receipt of a 1098-T form does not establish eligibility for certain educational tax credits. Similarly, students who do not receive a 1098-T because they do not meet the IRS’ reporting criteria should not automatically assume they are ineligible for these tax credits. Students should consult a tax advisor to determine eligibility.

What are the IRS’ reporting criteria?

The IRS requires Temple to provide 1098-T data for any student with payments received for qualified tuition and fees or Temple administered grants & scholarships during the current tax year. The following exceptions apply:

- Students who are not U.S. alien status

- Students who receive Temple administered grants and scholarships in excess of qualified tuition and fees billed during the current tax year

I graduated in did not receive a 1098-T form. Why?

tuition and fees during the current tax year and for Temple-administered grants and scholarships. For some students, payments for spring were received in November or December and included on the Form 1098-T for the previous tax year.

If you have any questions regarding this process or your 1098-T information, please contact at bursar@temple.edu or by calling (215)204-7269.

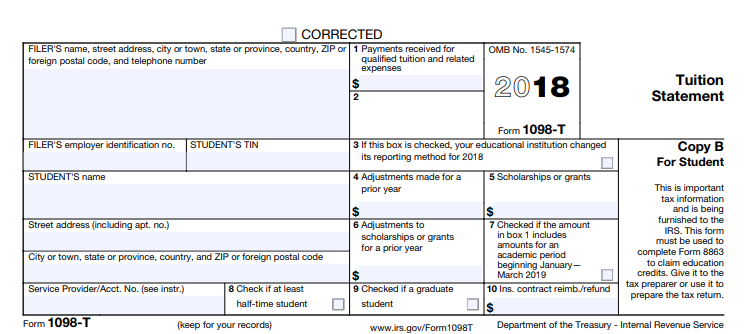

What does the current 1098-T form look like?

Which Boxes should be filled in, and what do they mean?

Box 1: Total payments received by Temple from any source for qualified tuition and related expenses less any reimbursements or refunds made during the tax year that relate to those payments received during the year. (Used by Temple starting 2018)

Box 2: IRS no longer uses (Prior to 2018, Temple used to report by charges billed)

Box 3: checked

Box 4: Adjustments made to a prior year's billed qualified tuition and related expenses (if applicable)

Box 5: Scholarships or Grants

Box 6: Adjustments made to a prior year's or grants

Box 7: Box is checked if there are both charges and payments for a future term received in the tax year.

Box 8: Box is checked if you are enrolled half time or greater

Box 9: Box is checked if you are a graduate student

Why isn't there an amount in Box 2?

The IRS no longer allows reporting of amounts billed, therefore this box is blank for ALL students.

What are "qualified tuition and related expenses" and what are not?

Qualified tuition and related expenses (QTRE) are those that a student must pay that are within the IRS guidelines. This is a chart of examples of Qualified Expenses vs. Not-Qualified Expenses for your reference. QTRE will show in Box 1.

|

Qualified Expenses |

Not Qualified Expenses |

|

Tuition |

Housing |

|

University Services Fee |

Meals |

|

Matriculation Fee |

Diamond Dollars |

|

Course Fees |

Late Fees |

|

Other Student Fees |

ID replacement fees |

I only have in Box 4 adjustments and/or Box 6 adjustments, what does this mean?

Adjustment amounts reported in Box 4 and Box 6, may change any allowable education credit you may have claimed for a prior year. We encourage you to seek the advice of a tax advisor for specific information concerning the handling of prior year adjustments.

Why aren't my payments for spring included in Box 1 (or only some of them)?

You may have only paid a small amount or nothing towards your spring semester in the current taxable calendar year (posted on the system between January 1st and December 31st). Any payments posted for spring after December 31st will be reported on the next year’s 1098T.

Am I eligible for a tax credit?

Employees of Temple University cannot offer assistance with tax form preparation, nor supply advice on what can or cannot be claimed. Please do not contact the university for that purpose.

The responsibility for your individual tax circumstances rests with the taxpayer alone, and Temple University is not responsible for your interpretation of this information. You are encouraged to refer to federal Publication 970 from the IRS.